Lyxfällan & Kronofogden

What is Lyxfällan and what is Kronofogden? Those are questions we need to answer in English before we continue discussing the topic. Lyxfällan is a Swedish show about personal finance, and revolves around Swedish people that are in high debt and with really bad spending habits. Also I found this blog post about the whole format being ripped off: Link (not sure if it is true, but it was an interesting read). Kronofogden is a Swedish governmental authority that enforces the collection of debt, both from and to private individuals and companies.

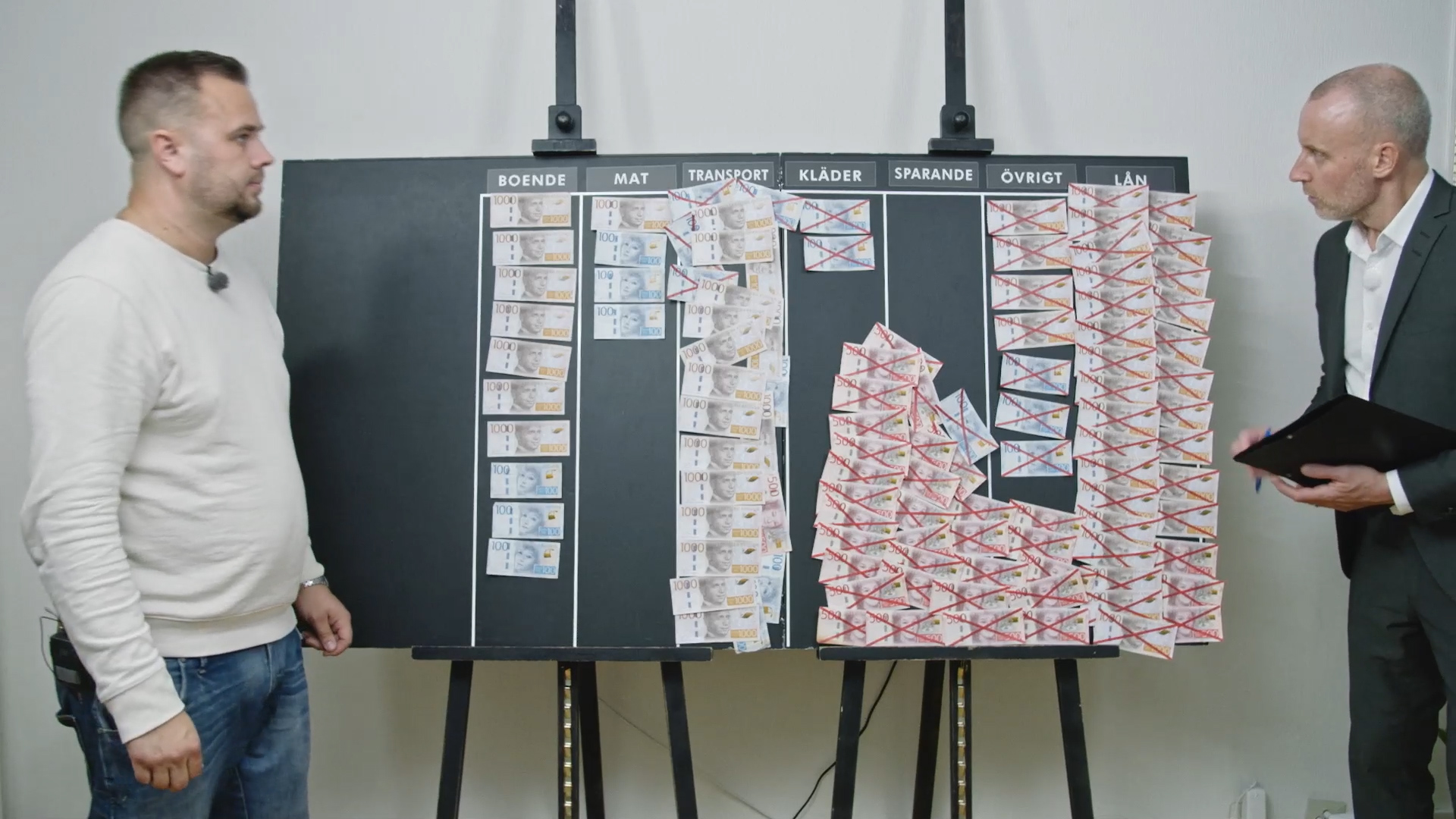

As someone interested in personal finance Lyxfällan has been one of my favorite "trash TV" programs to follow throughout the years. They have this big blackboard where they present the (often really bad) cashflow of the participants, and there is something about when a new record is broken - like biggest interest payment, or highest amount spent on food - that makes it so fascinating to watch.

Something that is brought up with the contestants frequently is how much money they owe via Kronofogden. Not to Kronofogden, as it is still the lender that owns the debt, but Kronofogden will enforce it by wage garnishments or even foreclosures. This puts the participants of the show in a predicament, because they are now forced to pay off the debt to Kronofogden first, as it will impact them the most. And sure, they have put themself in this situation on their own accord, so maybe some force and consequences are required - but what has become apparent to me over the years is how susceptible this system is to exploitation from dubious lenders.

During the shows many seasons we have been presented with a plethora of corporations that willingly lend money to the participants, even long after it has become apparent that they are not capable of paying it back responsibly. The root issues are often addictions of various kinds, mixed with an often very low income. Individuals which would often never be approved for a bank loan are happily being served by institutions with less than ideal lending terms. A couple of years ago SMS-loans were all the rage, but after some regulation capping the interest at 40(!!) percentage points above the reference rate, and later 20(still: !!) points they have cooled off a bit in popularity and the amount of marketing you see for them. They are of course still around, but mostly referenced to as "snabblån" or "fast loans". Either way, the trouble participants of Lyxfällan can get themselves into by using these lenders is still huge.

Klarna (which I assume you already know about) is the perfect case study for how the Swedish system is enabling predatory consumer debt. In Jonas Malmborgs book "Den stora kreditfesten" he discusses Klarnas expansion in to Germany in the early 2010:s, and how German lending practices and law made Klarna run with enormous losses. We can also see the same patterns repeating with the somewhat recent expansion in the USA, how big credit losses are on the books because of the lack of governmental enforcement. I don't care about the technicalities of German or American law - so this part only stands as an example of how other parts of the world handles it differently. But I don't think it is a coincidence that Klarna is fighting with American gigants like PayPal/Afterpay/Affirm etc. And no, its not because of their "superior consumer technology" or some nonsense like that. The whole checkout system was by the way sold off as a new company so that Klarna could focus on the core business of being a lender. To connect it back to Kronofogden: What I'm trying to say is that their early success was because of the Swedish debt-enforcement model.

How does Lyxfällan tie in to all of this? Of course the participants are directly affected by both Kronofogden, BNPL (buy now, pay later) companies like Klarna, and other predatory lenders. Historically the show has put all of the responsibility on the individual, and has made it out to be this big "moral failing" to end up in debt. Almost every episode of the "early" seasons pretty much ridiculed the participants for their (albeit, really bad) personal financial lives - and their lack of knowledge. Systematic problems has been totally ignored. It even went so far that the presenters of the show, the "experts", had financial ties to a Swedish niche-bank providing questionable loans. This seems to have changed as of lately, more and more episodes are being critical of the institutions lending the money instead of the individuals spending it. It is a refreshing take, as there is always going to be people that are (diplomatically) not so smart with their money.

To sum it all up: The Swedish system perfectly enables predatory creditors like Klarna and other "fast loan" providers to lend money to individuals with very very limited ability to pay it back, all because of Kronofogdens ability to reclaim a big portion of the credit loss.

Problematizing

Is this a very narrow way to perceive the system? Maybe. It leaves out all the economic growth the lending industry provides. It minimizes the personal responsibility we should apply to every individual. It probably cherry-picks information to create a narrative of the "evil" lenders that are in cahoots with the government etc. etc.

My YouTube feed is a never-ending stream of content relating to people getting in to huge debt in the USA. Caleb Hammer is basically the American YouTube-version of Lyxfällan. This seems to be a pretty big problem for "normal people" no matter how you twist and bend it. Are we enabling a healthy financial mindset by allowing people to make (what can snowball into) catastrophic financial situations - and then let them be bailed out by using tax-money?

Either way, I do not like the development. Why should corporations profit off of individuals misery like that?